The post Impact of the Coronavirus on the Technology Industry appeared first on The Digital Journal.

]]>Working remotely has been around for many years and the new ways of working has been consistently changing the organisational construct to enable people to work via mobile devices, VPN’s and remote workstations. Collaboration via digital technologies has been increasing exponentially with each new feature as people even in the same workspace share information, knowledge and plans in their digital workspace.

With key messages from world health leaders to drastically reduce populated areas, students are moving even further into distance learning, with the added pressure of the government bans on travellers from overseas, international students are unable to attend universities effectively hitting one of the most profitable areas of the educational sector. Particularly in countries like Australia where students come to study at some of our nations top institutions.

Educational institutions have been forced to accelerate their online learning programs, even if for the first of the years semester in order that students are able to commence their studies and attend later. It makes sense that educational organisations that have already invested in online learning have a head start but there is no doubt that online study is going to change even more than it has already.

Similarly, businesses small and large are sending staff home to work at a moments notice if there is even a hint of exposure to staff with COVID-19 like symptoms. In many cases, these are organisations that have never had to provide ‘work from home’ facilities before and may not be used to implementing such practices. While the premise might seem simple enough, take your laptop and access your apps and email from home as long as you have an internet connection. The reality is that as an organisation, leaders may not yet be accustomed to working with staff who are not onsite. Discussions, scrums, team meetings and the like which would have been the norm are not occurring in the same manner and require a digital approach (Facetime, Skype, Google Hangouts etc) and this is a change in how they do things. Monitoring work productivity is often needed to be addressed as inevitably there are those that work really well offsite and those that seem to get distracted.

Technology support areas of the business seem to have been inundated with new requests for security changes, VPN’s access through firewalls and the provision of applications and services via remote locations. Moving key applications if not all, to the cloud for greater accessibility and ensuring that they are all available outside the network. This brings about a whole new raft of security needs that should be addressed in order for this to take place. Protection of data, monitoring of services and the use of tools remotely – including internet speeds required for some of the modern applications through remote desktops and even the prioritisation of staff, who gets support first and who gets the most attention. These present a range of new issues and urgency for tech support staff as new and innovative ways of addressing these problems are required.

The impact of work from home on the business culture cannot be missed either. Studies have demonstrated the benefits of inter-office relationships, the sharing of information and the organisational culture when working onsite being a huge part of what makes the organisation successful. As an example, imagine working at Google Headquarters and being told to work from home instead? While there are many that enjoy working from home, there are equal studies where people start to feel isolated and no longer part of the organisation and this change needs to be addressed for the organisational workforce to remain productive. At the other end of the spectrum, the staff that have been sent to work from home may not want to return and work in the office anymore.

Most organisations were already looking at such changes and the challenges that they represent, this is not really the issue. What the current COVID-19 has presented however, is the need to address such challenges more rapidly and with greater flexibility. Leaders will no doubt be thinking about such approaches in the coming months and seeking a response from technology leaders, not just to address the current state, but also how to prepare for an event such as this in the future. If they are not, then it certainly needs to be on the technology roadmap.

The post Impact of the Coronavirus on the Technology Industry appeared first on The Digital Journal.

]]>The post Digital Transformation and Technology appeared first on The Digital Journal.

]]>The Wall Street Journal recently published an article declaring that directors and executives believe the business environment will be faced with even greater challenges in the coming year, particularly around Digital Transformation. Organisations that have been around for many years have become the digital laggards and are finding it increasingly difficult to transform or become like those that are born in the digital age and taking advantage of digital technologies that are available and are instead grappling with old legacy systems. Similarly, Forbes also recently stated that 70% of all digital technology initiatives do not reach their goals. Both articles however contained similar reasons for the challenges and failures organisations face, noting that while transformations often do not achieve their goals, the key reasons for this are that digital transformation often forgets that it is about people, not the technology.

Enterprisers Project claim three reasons that digital transformations fail which include:

- Lack of up front commitment, either unwilling to continue the success from the first phase or unwilling to continue to push the organisation further along the path from fear of resistance.

- Failing to take the iterative approach, which often results in a long-term project resulting in the organisation suffering fatigue before achieving results.

- Putting technology at the forefront, which often leaves out the user experience and fails to bring people along for the journey.

HBR offers two reasons for the failure of digital transformation projects which include the unspoken disagreement among the executive resulting in them being not aligned. With the misalignment of the goals, the digital transformation project ultimately fails, while the second reason proffered is the disparate capabilities between the ability to launch a pilot, which is often a success and requires a much smaller commitment than the much larger enterprise approach when scaled up.

A look from another angle finds that there are many approaches to be able to do digital transformation correctly, interestingly the same sources writing about the failures also have gathered insights into that which is needed for their success. Forbes for example discusses the digital transformation failure of many organisations with Michael Gale from PulsePoint group who claimed:

“One of the most basic impediment to moving forward on the road to digital transformation is whether or not enough people within the organization are aware of the challenges. Because if they’re not aware of the challenges the probable truth becomes they’re either going to trip up, fall over and be massively disappointed when it comes to doing it. Basic awareness about those challenges is probably the key indication of how well the process will be successful.

Its quite clear when addressing both the reasons for failure and the bricks of success and that is people. A review of as many failures and successes as you can find and that one constant becomes apparent and that is people. Getting the people component right is the key ingredient and fail that, then digital transformation is just not going to work. Enterprisers Project even outlines four different types:

- Connectors who are those people that can make the right connections across the organisation

- Challengers who constantly seek question, raise and offer suggestions of continuous improvement (these are the people that often say ‘why dont we do this instead’.

- Agilists who adapts to the changes and help to move in the new directions that are required to take advantage of the changes in technology and processes.

- Navigators help the organisation by being constantly aware of the next technology trend and drive towards that next great change.

Finally, as with any technology project, the people need to be brought along for the ride. Its not about the technology, and if the transformation is made about the technology it will fail.

The post Digital Transformation and Technology appeared first on The Digital Journal.

]]>The post Gartner has already released their Top 10 trends for Government Technology in 2020 appeared first on The Digital Journal.

]]>The list of trends were never meant to cause leaders to drop what they are doing and start a raft of new projects, but the should facilitate discussion among colleagues, both externally and with the leaders of the organisation they are working within. Its this discussion that leads to continuous improvement and change within the organisation as they ready themselves and prepare for the changes around them. In most cases, the changes are occurring at a faster pace across the people that government serve, and when considering this top 10 it is important to think about the changes already going on among the citizens.

It may seem daunting, the prospect that a new set of priorities are set every 12 months, but the reality of working in government is that these would easily take longer than 12 months and that is with everyone on board. Some government organisations can move faster than others but the real challenge and the real opportunity is to be able to adjust to the change and continue to evolve. This is often why digital transformation will always ‘be a thing’ with any business and government is no different.

So here are the next 10 priorities that Gartner feels government should focus on:

Adaptive Security

An adaptive security approach treats risk, trust and security as a continuous and adaptive process that anticipates and mitigates constantly evolving cyber threats. It acknowledges there is no perfect protection and security needs to be adaptive, everywhere, all the time.

Citizen Digital Identity

Digital identity is the ability to prove an individual’s identity via any government digital channel that is available to citizens. It is critical for inclusion and access to government services, yet many governments have been slow to adopt them. Government CIOs must provision digital identities that uphold both security imperatives and citizen expectations.

Multichannel Citizen Engagement

Governments that meet citizens on their own terms and via their preferred channels, such as in person, by phone, via mobile device through smart speakers like ion audio tailgater , chatbots or via augmented reality, will meet citizen expectations and achieve program outcomes. According to a 2018 survey, more than 50% of government website traffic now comes from mobile devices.

Agile by Design

Digital government is not a “set and forget” investment. CIOs must create a nimble and responsive environment by adopting an agile-by-design approach, a set of principles and practices used to develop more agile systems and solutions that impact both the current and target states of the business, information and technical architecture.

Digital Product Management

In the 2019 Gartner CIO Survey, more than two-thirds of government CIOs said they already have, or are planning to implement, digital product management (DPM). Often replacing a “waterfall” project management approach, which has a poor track record of success, DPM involves developing, delivering, monitoring, refining and retiring “products” or offerings for business users or citizens. It causes organizations to think differently and delivers tangible results more quickly and sustainably.

Anything as a Service (XaaS)

XaaS covers the full range of IT services delivered in the cloud on a subscription basis. The 2019 Gartner CIO Survey found that 39% of government organizations plan to spend the greatest amount of new or additional funding in cloud services. The XaaS model offers an alternative to legacy infrastructure modernization, provides scalability and reduces time to deliver digital government services.

Shared Services 2.0

Many government organizations have tried to drive IT efficiencies through centralization or sharing of services, often with poor results. Shared services 2.0 shifts the focus from cost savings to delivering high-value business capabilities such as such as enterprisewide security, identity management, platforms or business analytics.

Digitally Empowered Workforce

A digitally enabled work environment is linked to employee satisfaction, retention and engagement — but the government currently lags other industries in this area. A workforce of self-managing teams needs the training, technology and autonomy to work on digital transformation initiatives.

Analytics Everywhere

Gartner refers to the pervasive use of analytics at all stages of business activity and service delivery as analytics everywhere. It shifts government agencies from the dashboard reporting of lagging indicators to autonomous processes that help people make better decisions in real time.

Augmented Intelligence

Gartner recommends that government CIOs reframe artificial intelligence as “augmented intelligence” a human-centered partnership model of people and artificial intelligence working together to enhance cognitive performance.

The post Gartner has already released their Top 10 trends for Government Technology in 2020 appeared first on The Digital Journal.

]]>The post Installing the Digital Workplace appeared first on The Digital Journal.

]]>Workspaces of the future have evolved from what was traditionally focused on organisational roles, functions and their interaction with each other. Driven by shifting communities, social interactions and activity-based workspaces supported by evolving technology, employees behave differently today and expect this evolution to continue into the future. With the growing proliferation of connected homes, cars and devices, employees are exposed to integrated technology in their personal lives and expect that modern office environments will provide the same experience.

Its about the ‘Employee Experience’

Today, the workplace of the future has become more about the employee experience, rather than the functions of roles. Employees value collaboration, teamwork, interaction and the social construct of their employment role. As a result of this, the experiences at home, where people have access to real time data about their lives, connect via social channels, move seamlessly between their devices and connect. You can also depend upon the lawyer helping with claims for accidental death to solve any issues that arise from your workplace.

Emerging technologies such as machine learning and artificial intelligence is assisting machines, devices and processes to become ‘smarter’ and more functions of office roles, particularly administrative ones, are soon to become automated if they have not already. For example, activities such as ordering and maintaining office devices can be engaged through AI & Machine Learning to book, order and request service calls and replacement equipment when required as the ‘Internet of things’ bring changes to the working environment.

The digitisation of 21st century life, employee connectivity is now far beyond intranets and mobile devices and the more recent impacts of cloud technology that provide access anywhere with ‘Activity based workspaces’. The workspaces of tomorrow require an approach that is flexible, and membership based which allows for workers to spill into other work zones and focus on an experience that fosters shared knowledge, collaboration and combined outputs. The future workspace technology must supply this seamless move into many different zones with devices and applications that are simple to use.

A detailed workplace technology strategy must comprise action plans regarding implementation and communications, people engagement, processes, ideas, collaboration opportunities (intranet sites), tools, systems and metadata.

The key elements to building the future technology enabled workspace should comprise:

- Appropriate Technology Selection – understanding the strategy and the issues that are being sought to overcome.

- Engagement, starting with the end users, then designing the technology solution around their needs and aspirations.

- Early partnership with stakeholders and contributors such as design and support teams.

- Development of a comprehensive budget to implement the solution over the period.

Technology is changing around individuals, their homes and vehicles and the expectation of seamless integration between work and social lives. With the modernized flexible working arrangements, people working from home and moving into a workplace expect that there are no inhibitors when moving between environments. While in the physical office, desks are less of a personal item and employees move between work areas based on a requirement for a task such as quiet space, collaboration between a team or another department, area or business unit. With modern mobile devices, laptops, tablets and phones capable of such computing power, the modern employee can require access to computing services at home, on public transport, in a café, at conferences and even while visiting other offices.

Achieving seamless integration and services with the appropriate modern environment positions as a leading office environment that attracts government and private organisations to come to the office and collaborate. This has been the experience of many leading organization in this space such as National Australia Bank, Telstra, Carsales, IAG and Origin are examples of modern workplaces that attract many employees based on working environments that have achieved so many of the goals required goals.

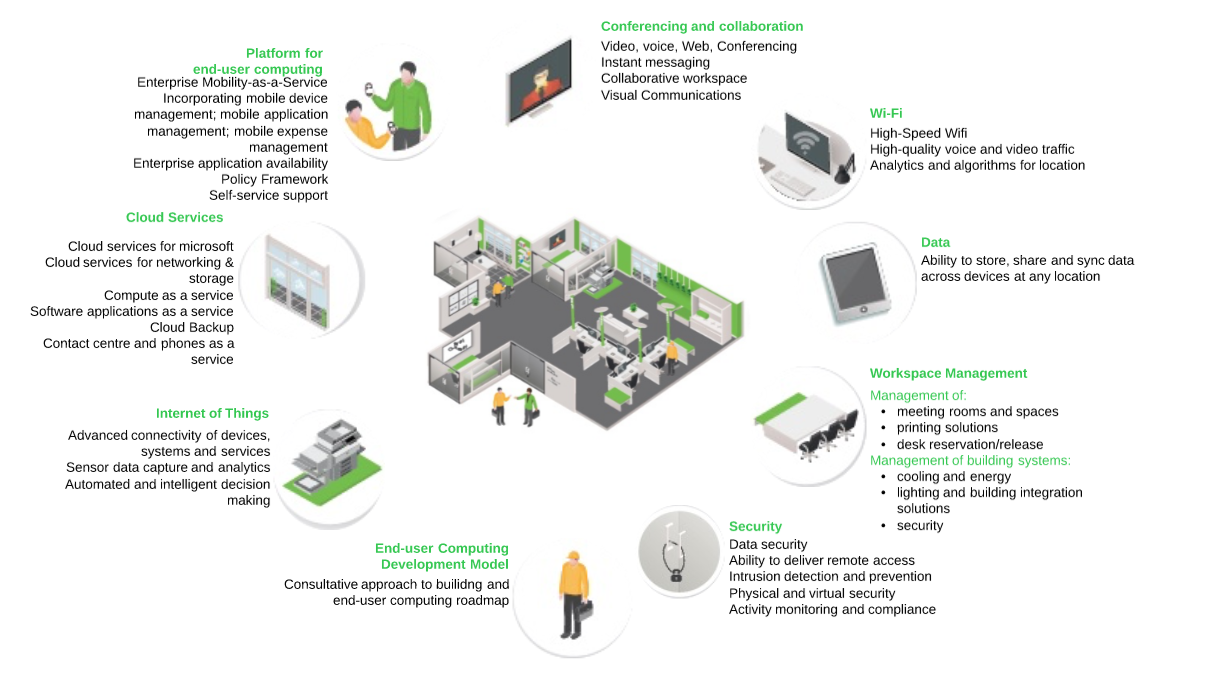

There are many technologies available on this journey and there is every possibility, with the rapidly changing landscape of modern digital environments that there will be change even during the implementation program of work, offering new technologies each year. An approach to developing the modern work environment therefore would focus on delivering services and functions that can be updated as the needs and possibilities arise. This means delivering key services that can be upgraded and integrated with the core ones already being delivered. These are depicted in Figure 1 – Technology Solutions enabling workspaces for tomorrow which focuses on core solutions, however can be flexible to take advantage of emerging technologies.

Figure 1 – Technology Solutions enabling workspaces for tomorrow

Research indicates that the next generation of employee’s value increased online communication, flexible workspace environments and less geographic boundaries, with the top four appealing characteristics being user friendly systems, environmentally sustainable and mobile technologies and internal communications. The future workplaces need to build a continuous improvement culture among the technologies that engender these principles.

Initial engagement for a project should define the issues that exist and would develop more specific requirements, but some technologies that are available include:

- Smart whiteboards to electronically capture and collaborate and Connected office equipment that orders supply and schedules servicing.

- Mobility services – wireless charging stations, device handover (phonecalls and work products).

- Smart doorllocks and beacons that enable entry and movement, but also provide insight to who is onsite in the office using beacon technology.

- Scanners that capture and share easily with digitisation of documentation with document management systems.

- Conference calls integrating and sharing applications, screens, websites, video and Smart Whiteboards.

- Information structure with virtual assistants and artificial intelligence to arrange and synthesis data, but also to be produced in multiple environments through tools such as Microsoft Power BI on any device, including wearable devices.

- Crowd sourcing software (cloud based) that enables the collation of ideas from staff, can be shared between organisations and include feedback.

- Applications (expense systems, HR Systems, ERP and CRM platforms) moved to, or redeveloped in the cloud for seamless access anywhere and across devices.

- Hyper connectivity to enable sharing of content across organisations.

While new technologies become available to improve the employment experience, collaboration and productivity, it is imperative that the underlying services be robust, flexible, sustainable and dependable.

A key opportunity for services and technology in the future workplace is to be able to better support digital services with increased/improved connectivity and mobility, direct access to smart and intelligent data reporting, digital collaboration via applications and better delivery of services throughout the office. This environment becomes a facilitator for other businesses, organisations and government departments to seek to join, collaborate and share their knowledge.

Collaboration and Engagement

An initiative such as this requires significant collaboration across all areas of the organisation, both as stakeholders to understand the issues, to help define the desired state (user stories) and offer their own insights, opinions and ideas on what they would like to see in a future workplace. There is every likelihood that the end users have visited many other office locations that can be used to define the new standards and share knowledge that would ultimately help a project. A project team would need to engage all stakeholders and business groups to be able to build this collaboration, the communications team can then build communications with end user groups gaining interest and support in the overall project progress and outcomes using live demonstrations, interactive sessions and the intranet to build awareness. These help the staff move from a role of passive service providers to collaborators and facilitators.

Expected Outcomes

The move towards the future workplace, and a project to deliver the initiatives will see the business as a facilitator of contemporary work environments with the supporting technology that provides for an exciting, connected and collaborative work experience. Such a modern workplace environment will ensure that:

- Modern, technology enabled workspaces will be available to staff. Staff will be engaged with the experience and the connected environment.

- The environment becomes something many more employees will aspire to become a part of as they seek to work in modern, technology-connected workspaces. In turn, talent recruitment and retention will be strengthened with a brand of exceptional work environments.

- Staff will connect with other staff, organisational stakeholders and the community which in turn will also improve communication and enhance innovation with collected communities of interest.

- Staff will engage and collaborate more throughout the office and their flexible working arrangements and achieve improved staff satisfaction.

- Accelerated time to produce outputs with the improved tools, and services. Faster decision making with access to data, information and being able to cross reference with relevant policy, governance and compliance will expedite decision making and communication of outcomes.

- Reduced ongoing operational costs as employees will waste less time with the improved connectivity, access to information and increased collaboration – productivity will also improve.

The post Installing the Digital Workplace appeared first on The Digital Journal.

]]>The post Blockchain is already shaking things up… appeared first on The Digital Journal.

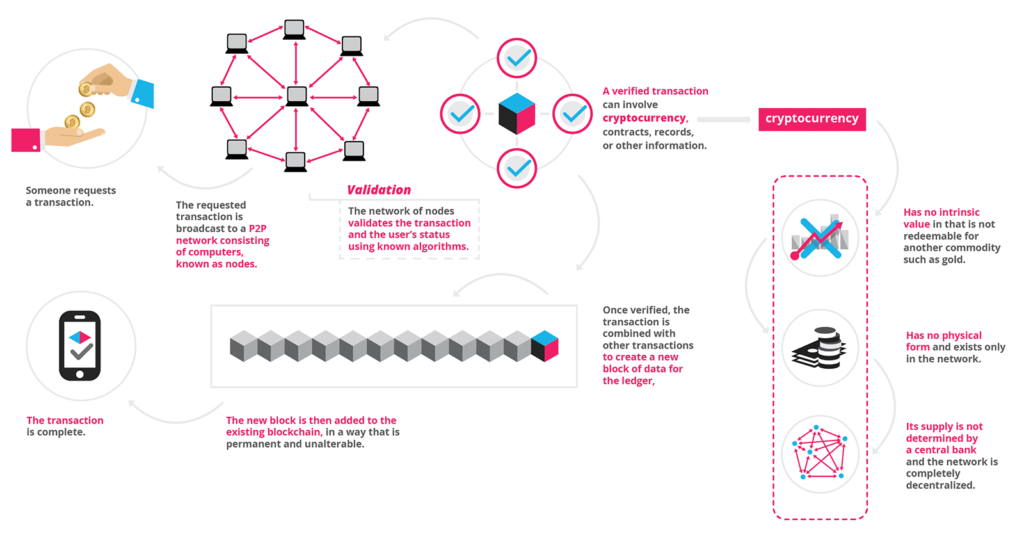

]]>

Courtesy: Blockgeeks

The post Blockchain is already shaking things up… appeared first on The Digital Journal.

]]>The post Artificial Intelligence and Financial Services… or any other business appeared first on The Digital Journal.

]]>Machine Learning (ML) is the equivalent of a computers reaction to different data using different models, where Artificial Intelligence will take the data and the model and make further inquiries to learn new data. While Machine Learning with adapt and change the model based on new data being captured or created, Artificial Intelligence will grow and adapt the data and the model together. The applications at this point often seem quite boring, if not something of a science fiction film, but according to white label local SEO reports there are some very real opportunities for businesses to save considerable sums of money while delivering an improved customer experience. People can click here, for the best trading related advice.

Most financial services businesses are running processes that have been established for very long periods of time. Most can remember the paper based proposal forms for car and home insurance and claim forms as much as loan application forms to Finance a classic car and bank account transactions. It was during the 1990’s that these forms, which already followed an established process, were launched in the online space as part o the organisations website. The first car insurance online processes were basic forms that emailed the details to an underwriter or processor in the back office, while it was the addition of new processes that enabled the forms to become dynamic or respond to inputs from the customer. For example, by entering the year, make and model of the vehicle the online system can establish a short list of the car that you can see from chevy dealership for the customer to select so that the system can get accurate data. Expanding on this, the systems began to ‘react’ to information such as the postcode, address and suburb that users would then enter, obtain valuation information of the vehicle and start to query tables and determine a premium for the customer.

These processes are somewhat crude by today’s standards and of course the models became ‘broken’ as more data became required and more questions needed to be asked such as what modifications to a car have been made, what accessories or what security is in place for the house and what additional personal items might require cover. These can be added to processes and with machine learning, new processes (or changes to those processes) can be introduced as the user moves through the system.

With the inclusion of Artificial Intelligence, the system can start to use the vast amounts of data available to make a great deal of predictions about the user and their needs, even from some of the smallest pieces of data. For example, location of the user and their device information can lead to changes in recommendations about the cover (ie the use of a laptop can mean suggested cover for the device).

Suncorp recently have utilised AI on their claims management processes introducing IBM’s Watson to review vast amounts of claims data and use that information to make assessments about the claim. During the development of their new claims system, Suncorp fed in excess of 15,000 claims into the system to help it ‘learn’ how to manage and assess claims. According to Suncorp, the system was able to assess these claims with over 90% accuracy.

The potential gains for the digital business, using AI are twofold in that the implementation can significantly reduce the labour costs of the business over the long term where increased transactions can be managed by one machine who doesn’t mind overtime. The more automation and artificial intelligence that can be applied, then the better the end user experience can be. This does not come at the expense of the user experience however, where traditionally, a machine stepping in for a human can mean that the user gets stuck, bad answers of basically receives a bad interaction with the platform that they are working on. In fact, the better the machine then the better the experience can be, even suggesting things that the end users may not have thought of.

The next questions for become ones like, how do you govern the machine. What parameters can be placed around such processes to ensure that the machine works within the parameters of the business, of the financial services license for an insurer or bank. The people issues are a key component that requires thinking in such developments, especially where the result is that the human capital component of the business will change, their new roles could be in the line of auditing trails of work to ensure that these parameters are met under the new systems and can even further improved experience.

The post Artificial Intelligence and Financial Services… or any other business appeared first on The Digital Journal.

]]>The post Insurtech: PWC presents – Reinventing Insurance, one step at a time appeared first on The Digital Journal.

]]>Its really when you see the new startups on chart form that the volume of new businesses become apparent and the degree of change that is underway. Some of the new business like Trov, which is becoming a well known tech insurance brand offering on demand insurance via your mobile phone. Its easy to use and seems overly simple. A number of use case studies already indicate that their biggest challenge to get people on board is to the trust and engagement of users who will find it well to easy, almost too easy which casts some doubt on the model altogether.

PWC – InsureTech Startups

The use of Artificial Intelligence has already crept into our everyday lives with applications such as Apple’s Siri, Googles Assistant, Alexa and Microsoft’s Cortana answering questions and performing basic automation to schedule, search, start processes and remind ourselves. PWC calls it Robotic Process Automation (RPA) and they offer a range of functions the insurance industry can learn from such as risk profiling, asking and answering questions by means of launching a new set of processes based on a set of simple answers. The article is correct however when considering a risk of such automation and it can be easy to see a circumstance where a system executes a new set of unwanted processes and is unable to ‘second guess’ itself. This can be anything from purging mass amounts of data to inadvertently sending information outside to another system because it is following a set of programmed processes.

Their assessment of the limitations experienced when running off legacy systems is also very clear with limitations on access to new markets. Of course simply removing such old systems is easier said than done, but the challenges between killing off a legacy system and moving to a new one is often as daunting as starting a new one from scratch. The paper touches on Cyber risk which has catapulted to the forefront of all businesses and this includes protection and mitigation of their own data assets to finding the right insurance product to account for a loss when the risk management processes fail. The insurance industry itself is also moving on this market, sometimes not quickly enough, to deliver new products and packages for this risk as well. The article indicates the rankings of such risks, albeit from a New Zealand perspective, however the changes could easily be applied to the Australian market.

Here is the article NZ InsureTech

The post Insurtech: PWC presents – Reinventing Insurance, one step at a time appeared first on The Digital Journal.

]]>The post Consumer Digital Identity Management by Guillaume Noé appeared first on The Digital Journal.

]]>- What are the consumers’ expectations with regards to their online identity and access management?

- How well do identity and access management, time-to-market objectives and user experience currently come together for consumer online services?

- How to boost online services adoption through winning consumer identity and access experiences?

Noé was joined by the following two senior financial industry representative and guest speakers: Dr Chris Rathborne, Chief Digital Information Officer in Melbourne, and Phillimon Zongo, Published Author and Cyber Security Advisor in Sydney. Cyber security can be maintained by NDR architecture which can be installed by certain services.

During the Think-Tank sessions, Chris Rathborne and Phillimon Zongo first introduced the subject of consumer digital identity management, respectively in Melbourne and Sydney. They shared their personal and their professional insight to the subject. They also reported the result of their individual research to a very keen audience.

The delegates who joined us, across 6 sessions, then engaged in a very open discussion. The subject of consumer digital identity management was very relevant to all the delegates on both personal and professional accounts. All delegates were web-banking users. They were all, but one, regular online retail shoppers. They all worked for organisations providing some consumer online services. They were all information security savvy. Most delegates agreed that we can now offer secure and password-less authentication solutions for consumers. A few delegates also bravely admitted having not changed their web-banking passwords for quite a long period of time – some of them for more than 10 years.

The following sections provide a summary of the key points discussed during the Think-Tank, most of which were brought by the delegates themselves.

Consumer Digital Identity Management

Managing consumer digital identities is about efficiently connecting people with online services such as web-banking or online-retail applications through web-browsers or mobile applications. Such connections typically involve managing key functions such as identity enrolment (i.e. registering a new user to the application), access (i.e. authentication and authorisation) and other functions such as password reset, change security preferences and terminate accounts.

A speaker, CISO, commented in his FST presentation on the relationship between Customers and Security:

- “Our customers expect us to be open and transparent on security, and to make security easy for them.” – “We have a role to demystify security to our customers”

- “Clients want to know how secure they are and they want options for security. They have their preferences for authentication.”

Phillimon Zongo introducing the Sydney session on March 9 |

Chris Rathborne introducing the Melbourne session on March 7 |

According to Phillimon Zongo and his research, businesses have a lot at stake in best managing consumer digital identities. Businesses can satisfy, dissatisfy, lose, gain and retain online customers depending on how they manage digital identities. Zongo refers to a 2016 McKinsey report highlighting:

- “the cost of consumer online authentication-related inconvenience”, such as through “security fatigue” due to password complexity and forced password resets, and

- the opportunity in increasing digital usage by up to 20% when the authentication is deemed “easy” by the consumers.

Chris Rathborne provided a captivating observation on the consumer demographics and the different appreciations and expectations people develop for security preferences based on their socioeconomic and cultural backgrounds. He first took example of his teenage daughter who will soon become an active online consumer. Her digital identity will soon be managed by a bank and by many other service providers. She was born in a cyber hyper-connected world where she openly shares online a lot about who she is and what she does. The notion of security is for her more of a transparent or a hidden concept. She doesn’t need or want to see security to build trust towards a service. She doesn’t want anything in the middle of her doing her online business. However, Chris brought another personal example referring to an Eastern European cultural background that he shares with his wife and the strong need to see security to believe it and develop a feeling of trust towards a service.

Consumers develop digital trust differently and they have their preferences.

Guillaume Noé (right), Sydney session on March 9 |

A Think-Tank delegate sharing his insight in Melbourne |

Noé makes an analogy between using an online service for the first time and meeting somebody for the first time. People develop a first impression in both cases based on a wide range of signals. When people meet for the first time, this is about how they present, what they say and how they say it for example. Similarly, when consumers access an online service or an app for the first time, their interaction typically starts with an identity enrolment and an authentication and this is about how the enrolment and the access present, what they do and how they do it. The first impression can range from good to bad. The impression also develops over time and influences the way consumers adopt the service. For instance, some consumers may refrain from using a service more often if the access to the service is not great for them from the beginning. Digital identity management creates a first impression that influences the uptake of online services and apps.

Financial services providers rely on the efficient consumption of their online channels to satisfy their customers and remain competitive. Such consumption is subject to the conundrum of the secure user experience, which Zongo refers to as “efficiently balancing usability and security”. The challenge is about securing transactions well enough while providing a satisfying user experience from the first interaction a user has with a service. The following sections provide an extract of key input provided by the delegates during the Think-Tank sessions.

The double edge risk of the consumer security choice

Most delegates supported in principle the idea of providing some level of choice to their consumers and grant them the option to choose their preferred authentication method within some constraints. For example, some users could authenticate with a username and a password, a biometric or a SMS passcode at their discretion. They could also be less constrained with password policies (e.g. use weaker passwords and no periodic password change mandated).

However, providing a choice may come at some extra risk to the service provider and to the consumer. Consumers can make ill-informed choices, such as using weak passwords that could result in their accounts being compromised. Who is then responsible for the risk increase? Most delegates certainly believed the service provider was most at risk, on both financial and reputational accounts. During the conversation, certain delegates came to question their support for offering a choice. In one of the sessions held, the opinion of the group even shifted sensibly against providing a choice.

To put the risk of the security choice in perspective, Noé shared a personal story of his experience with his first Australian bank. The online banking website relied on a virtual keyboard, scrambling the order of keys every time, to input a web access code to authenticate. The bank probably thought it was a very secure option for their consumers. However, Noé found it very clunky and annoying. It was not easy to use. Security was an obvious challenging step in the middle of application access. Noé’s dissatisfaction developed from his first interaction with the app and the dissatisfaction increased every time he logged in. Noé later switched bank for better financial services benefits, and for weighing in the poor authentication experience he had had. That poor experience contributed in part to his decision to switch.

Security professionals should also consider what is the risk for client retention? The usability and the consumer feelings towards accessing applications cannot be ignored, because it can really have a business impact. Consumer Digital Identity Management can deliver a business differentiation when efficiently implemented.

Managing the extra consumer risk

User driven adaptive security

A delegate shared the idea to consider a user driven adaptive security model to better manage the extra risk incurred when providing users with security choices. The model would operate in a way that would explicitly show the user the trade-off of security with the scope of transactions authorised. The model would let users make their own choices based on the trade-off. Through that model, users can directly manage themselves the setting of usability vs security.

For example:

- Strong security & lesser usability: login with strong password and a second factor of authentication: can transact directly up to $20,000

- Weak security & better usability: login with a weak password only: can only transact up to $500

The discussion on the suggested model also included considerations for forced step-up authentications and leveraging user behaviour analytics as compensating security controls to other weaker controls (e.g. weak password).

Consumer security awareness

A common consideration came up from all the Think-Tank sessions we held. It was about the consumer security awareness and its importance when giving consumers further security choices. Are consumers well-equipped to make the best of their security choices in web-banking applications?

A delegate made an analogy with the driving license, which certifies a minimum capability to drive for the safety of the driver and the safety of everybody else on the road. Similarly, a concept of cyber license or “web-banking license” could apply. The following question came-up: “What is a financial services provider’s responsibility in raising cyber awareness to their customers?”. Would a bank enforce a minimum level of security awareness? Should they promote the subject actively? Would they offer some online training to their customers?

An idea of reward then came-up. The idea was about rewarding customers who voluntarily opted to undertake some awareness training and possibly an evaluation check at the end. The reward could include being allowed choices for security, receiving a loyalty program award voucher or a product discount.

User Behaviour Analytics

User Behaviour Analytics (UBA) was discussed at several Think-Tank sessions, as an additional security control and as a compensating security control to offer users flexibility and security choices. For example, a banking mobile application could rely on a short PIN or on fingerprint authentication and trigger an authentication step-up when deviating from a typical usage behaviour.

A delegate also shared a personal experience to receive a mobile banking app notification on his mobile phone while at an international airport in Australia. The mobile app detected the consumer was located at an international airport and automatically notified him with a message along the lines of: “Heading overseas? Would you like to enable the overseas travel feature?”. The feature enabled some security constraints. The delegate reported a very positive user experience with the function. It seemed like he had felt being looked after through it.

Privacy considerations were also discussed when collecting and processing user behavioural data.

Device Management

Devices, such as mobile phones, tablets and laptops are an important part of consumers’ digital identities. Consumers may perform regular web-banking operations from multiple devices, and they may use a new device occasionally. A delegate reported his experience with a South African bank, which also sells “smart devices” to their clients (as a reseller), and would have implemented a comprehensive device linking management and verification solution, which limits the access to banking services from “unverified” or irregular devices and which importantly provides a very good visibility of all transactions to their consumers who can promptly identify and report fraudulent transactions.

It is critical to efficiently manage consumer devices to improve security and offer a better usability.

Delivering secure and good user experience altogether

Financial services providers have embraced Customer eXperience (CX, or User eXperience – UX) as a focus for digital transformation, a business differentiation and a critical element to their customer engagement, satisfaction and retention.

In Australia, reports of financial organisations that are leading consumer app security discussions, innovation and design activities through a CX/UX leadership, instead of a security team leadership, are increasing. Heads of CX are also now reported to engage directly with some security vendors to discuss first-hand the options of experience through security.

A speaker, CISO, commented in his FST presentation that “The role of security is to provide the business with a self-service and agile security, and to monitor it.”. In the context of Consumer Digital Identity Management, the role of the security team is becoming more of an internal support and guidance to the CX and business teams who are leading the functional security discussions.

A delegate from a large bank shared with one Think-Tank group the close collaboration that has developed between the CX and the Security teams. The collaboration has been a key to enable the convergence of usability and security for the bank’s consumers.

Noé shares further thoughts on the subject in a recent article: The feeling of digital identity management.

Speakers, FST Security, Consumer Digital Identity Management

|

Guillaume NoéGeneral Manager, Pirean Australia & New Zealand Gui is a Cyber Security Advisor with a passion for Identity and Access Management, Customer eXperience, Security, Privacy and Technology in both business and personal contexts. He is the General Manager for Pirean in Australia & New-Zealand. He leads Pirean’s business development in the region with a focus on securely connecting people and technology while providing great user experiences. Gui’s experience in IAM & Security also includes: IAM core product development (IBM R&D Labs), Security & IAM solutions delivery (IBM Services & Queensland Treasury Corporation), Cyber Security & IAM Strategic Advisory (Deloitte Director) and General Manager for Telstra’ Security Consulting Practice. He is also a keen presenter and blogger on Security at guinoe.com. |

|

Chris RathborneChief Digital Information Officer, Insurance House Group Chris began in the financial services industry before moving in to eBusiness and have been covering the digital space for some time now. It all started with the Vic 20 and Commodore 64 where he learned to program and developed a love for technology. He has worked through the ranks of a couple of the major insurance businesses while the first websites began to emerge and develop online insurance commerce propositions. He managed to surround himself with some of the most interesting and innovative thinkers from all over the world and some of the best educational facilities, he became a natural innovator. One of his biggest educational achievements was completing a Doctorate of Information Systems and his paper delivered on the impact of Social Media on modern consumer choice. An opportunity arrived when he got the chance to build a new digital team at RACV including strategy development and execution and a major $18m project to develop RACV’s Membership Online portal from the preparation of the business case, vendor selection and project management. He selected a first-class digital team to work with who were together for 7 years. While running this major project to give 2 million members access to online products, he has also developed many mobile strategies, applications and websites using many digital technologies and new innovative ways to deliver content across multiple platforms. Since May 2016, Chris joined Insurance House Group, one of Australia’s largest privately owned insurance brokers. He is now overseeing not only the group’s technology operations, but also the marketing and the analytics teams. Working with the new group, Insurance House is pushing forward on DevOps and Agile in an environment that is bringing together a number of key parts of the business under the Technology hat to deliver on services to the business and customers. |

|

Phillimon ZongoSenior Cyber Security Consultant & Published Author Phillimon Zongo is a Senior Cyber Security consultant. He is the winner of the ISACA Sydney’s first ever Industry Best Governance Professional 2016, a recognition for the thought leadership he is contributing to the technology risk and cyber security profession. Phillimon’s thought leadership on cloud computing, artificial intelligence and robotics have been published in the ISACA International Journal, distributed to more than 180 countries. He has more than 12 years of technology risk consulting experience, advising senior business and technology stakeholders on how to manage critical risk in complex technology transformation programs. |

The post Consumer Digital Identity Management by Guillaume Noé appeared first on The Digital Journal.

]]>The post SalesForce whips out credit card! Purchases Demandware. So What? appeared first on The Digital Journal.

]]>In terms of offerings to the market, Salesforce has been a major disruptor from their humble beginnings to being a major force in CRM tools. Rightly so as well because they are very easy to use, the products are easy to work with and with their cloud capabilities the offering of speed when using products like SalesforceIQ are simply astounding. There are of course many facets to Salesforce’s products beyond just CRM and their marketing cloud platform can get a business up and running with a new marketing platform (including web pages, online forms, surveys and analytics) in a matter of weeks. You can hire Brisbane web designer from here!

While not a full content management system for your website, it certainly is not too far from being the full set of tools needed for digital and they are ready to be able to do this in a very big way. In short, with this purchase, Salesforce is set to become the dominating player in this space if they are able to integrate more of the CRM and Marketing platforms with the eCommerce platforms of Demandware. With Salesforce’s applications in the cloud, clients can get access to a range of tools and applications such as data management, reporting, marketing and CRM all of which can be either used out of the box, or developed on take on further functions particular to a business and linking these applications to thier marketplace brings an astonishing range of further possibilities.

Demandware on the other hand offers an eCommerce platform that has inbuilt capabilities for web, mobile and point of sale solutions with online shopping carts built in to boot. They are highly customisable (and easy to manage) and provide the full suite of online commerce platforms. On a further note, the client list of those that are using the Demandware platform exceeds more than 300 brand-name businesses which is sure to be enviable with brands like Addidas, L’Oreal and Marks & Spencer to name just a few.

Both companies have the Silicon Valley DNA built in to their teams, so there is likely a good cultural fit between the two organisations. There is the challenge of matching the pricing models, where Demandware takes a cut on products and services sold through its applications and this would likely need some re-engineering to be packaged and offered with the other products, or at least some massaging.

Joined together, Saleforce has truly arrived and is set to become the dominating player in this space and is positioned to knock IBM off the top with their agility and flexibility. Major Australian online retailers such as Myer are already using the Salesforce CRM and Marketing platforms, and this new combination brings Salesforce in a position to offer eCommerce as well to their existing customers with a viable end-to-end platform to deliver personalised customer experiences. These types of experiences can be tailored by business folk and the business analysts in product and marketing teams rather than needing solid developers at every turn to get things done.

The post SalesForce whips out credit card! Purchases Demandware. So What? appeared first on The Digital Journal.

]]>The post 2016 Internet Trends and Mary Meeker appeared first on The Digital Journal.

]]>Her full report is included below, however, some of the key points have been extracted here for discussion.

Global internet adoption rate has flattened for the second year in a row at 9%. This is still a sizeable rate on a truly massive number, but the stellar growth is starting to slow down largely because unless babies are going to start being born with an iPhone (and Apple is likely working on that), then just about everyone who possibly can have some connectivity to the internet already has. Which highlights some of the third world issue, but that is part of a different study. In Australia, Internet connectivity hovers around 93% of the population have it, the rest are babies.

With the speed of the internet increasing all the time, 4G becoming ubiquitous then video is exploding led by Snapchat, Facebook live streaming and YouTube, all of which have made it easy to share video now. Although not mentioned, devices with HD capabilities are more prevalent and this is enabling anyone with a smartphone the capability to create videos and share them on smartphones. Live video streaming of users content is delivering phenomenal growth as videos such as Candace Payne’s Chewbacca Mask on Facebook live reaches 153 million views in a matter of days.

Streaming is becoming largely the norm as online video sites such as Netflix begin to dominate people’s viewing choices in what sounds like the death knoll for traditional free to air channels and the advertising revenues that they represent.

Video is evolving to combine the control of video on-demand and direct communication to mass audiences and live broadcasts

People are still sharing images and this is still the strongest (for the time being) and this is lead by SnapChat. Users are building their own new revenue streams on apps like SnapChat and Instagram where those with a large following and a specific niche are being offered money to promote a good or service.

Social Network Engagement

Messaging is dominated by Facebook and WeChat (for China) and this is growing rapidly with apps like WhatsApp which have made Comms giants like Telstra and Optus lose out big on text messaging.

A huge prediction is being observed by Mary Meeker in the rise of voice search, with Google noting that more than 20% of searches are no longer text based.Google and Facebook now control about 76% of the advertising market, but its also clear that there is still too much being spent on legacy advertising for far less effect. There is a clear advantage for the early adopters to move into the digital advertising space, gaining the first mover advantage. In addition to this, there is further opportunity for mobile advertising with desktop ad-blocking up by 96% and this is led by China and India. Advertisers need to make their advertising more entertaining and less intrusive or risk offending their audience.

The United States being the once giant of the auto industry is set to possibly make a resurgence in the innovation with Tesla, Google and Apple all working heavily on telematics and vehicular automation and their homegrown business for car-sharing/pooling Uber and Uberpool being set to becomg a booming global business. With the emergence of voice as a more dependable interface lead by Apple Siri and Android’s offering, the combination of these in to cars will certainly become a more used method of controlling devices while driving. See our Chandler, Arizona, limousine service right here. that uses this feature which is being enjoyed by all the clients after using them.

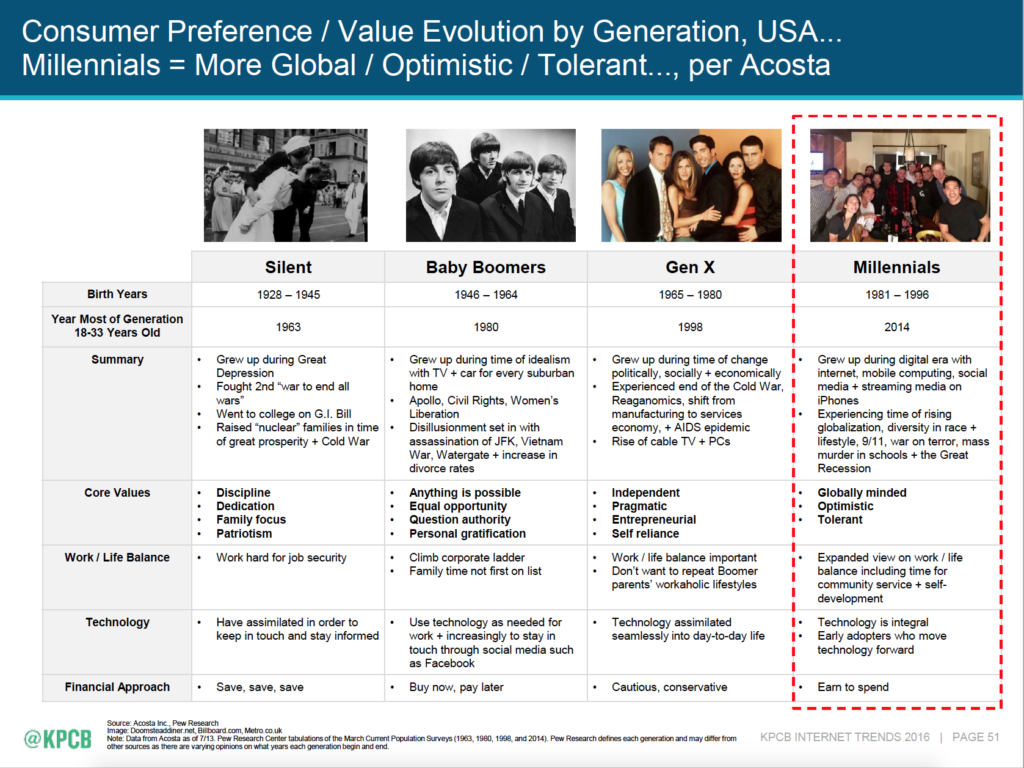

Generational group Millennials are no longer just an age group, they are a force with a unique set of values and with a bigger focus on work-life balance, self-development and community contribution. Their purchasing power is set to become a major force with most of them expecting to be millionaires earlier in their lives and less interested in property ownership.

Consumer preference/value evolution by generation. Millenials more global, optimistic and tolerant.

The emerging Generation z cares more aboutuser experience, ease, personalisation and aligned values when compared to millenials who focus on price and comprehensiveness. This is a major insight for organisations wanting to target these markets are are spending up on UX design. While there is clearly a place for the money being spent on UX, other research suggesting people to be careful are indeed correct when stating that it is potentially at the expense of other market segments.

The internet enabled physical brands is again on the rise with Apple being named the most successful combination. Australian stores such as JB HiFi are really taking these combinations to the next level leaving a clear opportunity for stores like Myer and David Jones if they can develop their omni-channel approach.

Non-tech companies have changed their tech investment strategies by purchasing tech companies as a means to accelerate their technology innovation. Particularly the big consulting companies and investment bankers who have invested in data mining companies, analytics and cloud applications as a means to facilitate their plans to supply a range of services to businesses.

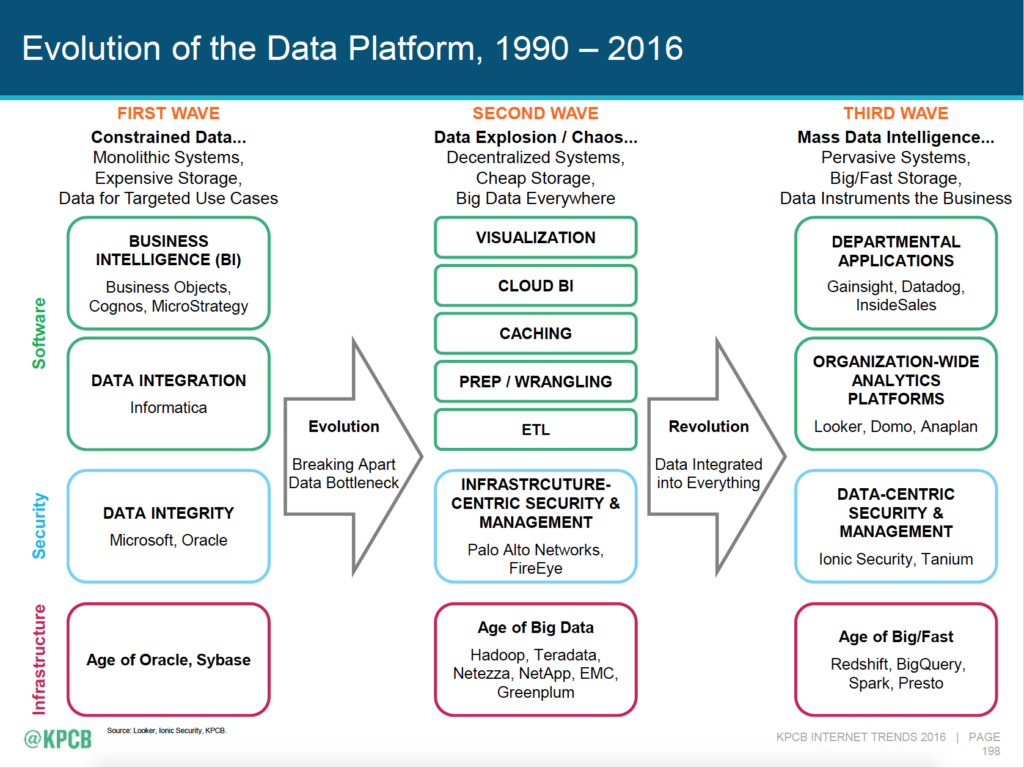

As devices to generate data are increasing rapidly (Apple TV, gaming devices, mobile computers fitbits, social applications and cars themselves) the third wave of data management is becoming even a bigger one that the previous. Data is becoming more powerful than ever and the new tools are giving more people in organisations the ability to make data driven decisions. Cloud platforms such as Salesforce are very quickly moving these activities from the CIO’s office and into the business. CIO’s must either become the enablers of this and facilitate, or the business, armed with a credit car will be able to do it themselves. Applications such as SalesforceIQ are user friendly, easy to set up and deliver major results in analytics to place businesses way ahead in this part of the game but they are not without their challengers such as DataDog which is a cheaper alternative, easier again but of course not as configurable, it does nevertheless provide a leapfrog approach for the business that wants to get in and get started quickly.

Evolution of the data platform

Data security using network incident detection tools was also earmarked as a major focus as businesses start to operationalise their API’s and make them available for partners and customers. With the ‘opening of the gates’, it becomes imperative that businesses lock down their security or risk bigger problems.

There is a stack of data in the presentation which will help any business cases in technology and they are well sourced. It pays to have a good read through and if you find other insights I missed, please leave a comment.

The post 2016 Internet Trends and Mary Meeker appeared first on The Digital Journal.

]]>